यह भी देखें

04.03.2026 02:02 PM

04.03.2026 02:02 PMJapan's energy security moved to the forefront after the US. and Israel struck Iran, forcing previously dominant items on the agenda — wage negotiations with unions, reforms and consumption tax, and the Bank of Japan's policy rate — to the sidelines. Suddenly far greater stakes emerged: the threat of a sharp rise in inflation, a slowdown in GDP growth or even a slide into recession and a collapse in the stock market.

According to Japan's Ministry of Finance trade statistics for 2024, 95.1% of the country's total oil imports originate in the Middle East, and 94.6% pass through the Strait of Hormuz. Calling this a critical dependence is an understatement.

For now, the threat is limited — at the end of December 2025, Japan's oil stocks amounted to 254 days' supply, of which 146 days were held in government reserves and 101 days in private stocks. The risk of a supply shortfall is still low, but the longer the war continues, the deeper and more lasting the consequences will be.

The LNG picture is the opposite: supplies from Qatar account for only about 4% of the market, so a halt at a Qatari facility would have minimal impact, if any. Yet LNG inventories cover only about three weeks because of storage constraints, and gas prices are surging. Japan will not be spared.

Thus, there is no immediate, manifest risk of an energy crisis in Japan, but if the conflict becomes protracted, that risk will grow. At the same time, the threat of stagflation is rising because the government may be forced to stimulate demand. On March 3, Reuters reported that, according to its sources, the Bank of Japan will refrain from raising rates at its March 18–19 meeting.

In the short term, one should assume that higher energy prices will contribute to yen depreciation, and that depreciation in turn increases the risk of currency intervention. If depreciation is, however, necessary to preserve the balance of payments, the government may decline to intervene even if USD/JPY rises above 160.

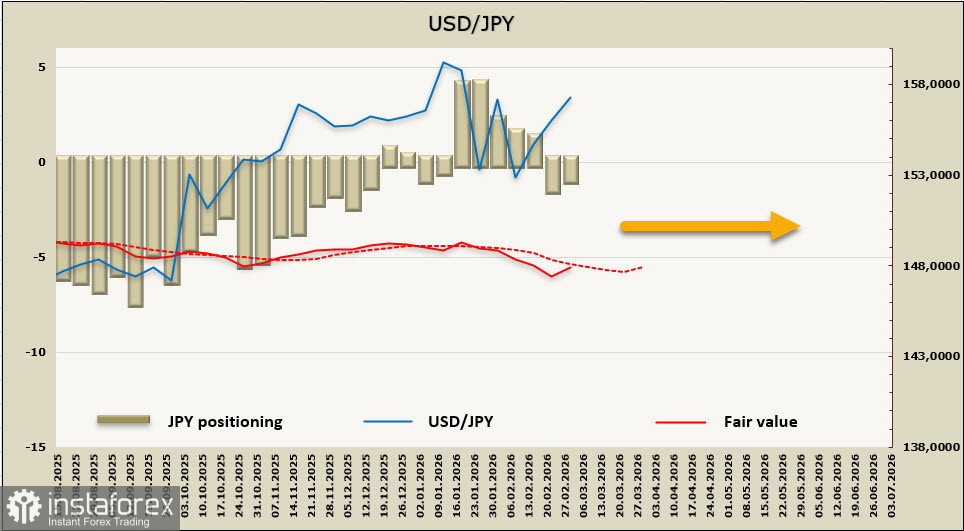

Net speculative long positions in the yen fell by $131 million over the reporting week to $0.93 billion; positioning is neutral, the implied price remains below the long-term average, and there is no clear directional bias.

The yen's dynamics under current conditions are driven by short-term factors, while longer-term considerations such as the Bank of Japan rate have receded to the background. The prospect of interrupted oil and petroleum product supplies and rising energy prices would inevitably lead to an inflationary shock, continued declines in the stock market, and threats to economic growth. The probability of currency intervention has fallen; the market may need some time to reprice the situation. For now, a move in USD/JPY toward 160 appears more likely in the near term than a reversal to the downside.