یہ بھی دیکھیں

09.06.2026 07:37 AM

09.06.2026 07:37 AMThe dollar slightly ceded positions yesterday, even amid the further escalation of the geopolitical situation that traders have become accustomed to lately.

Even reports of successful Iranian drone strikes on two U.S. bases in Iraq did not spur the dollar to continue its rise. It seemed that the market had already priced in an initial reaction to the escalation of the conflict and was waiting for more substantial catalysts to change the correlation.

The situation was aggravated by statements from U.S. President Donald Trump, who reportedly threatened Israeli Prime Minister Benjamin Netanyahu that he would leave him to face Iran alone if the escalation of Israeli attacks led to full-scale war. This sharp rebuke from the American administration, which traditionally supports its Middle Eastern ally, caused confusion in financial markets. Uncertainty about the future of U.S. policy in the Middle East cooled investor interest in risk assets, but the dollar, contrary to expectations, did not receive the anticipated boost.

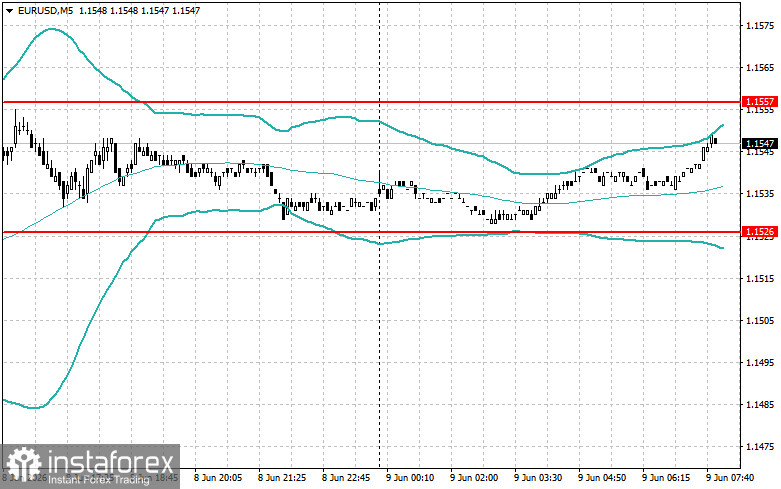

Today, the first half of the day promises to be busy for financial markets, especially concerning the European economy. Key macroeconomic indicators from Germany are expected to be released, traditionally exerting a significant influence on the euro and investor sentiment. First and foremost, this includes data on changes in industrial production. This indicator is among the most sensitive to the business cycle and can provide a clear picture of current dynamics in the largest economy in the Eurozone. Weak figures could increase concerns about a recession.

Alongside the production data, figures on Germany's trade balance will also be released. This reflects the difference between exports and imports of goods and services. A positive balance is traditionally a strong point for the German economy, but a reduction or shift into negative territory could signal declining competitiveness of German goods in global markets.

Today, we also expect a speech from European Central Bank President Christine Lagarde, although it is not yet known whether she will address monetary policy. However, amid rising inflation and slowing economic growth, every word from the ECB head will be closely scrutinized.

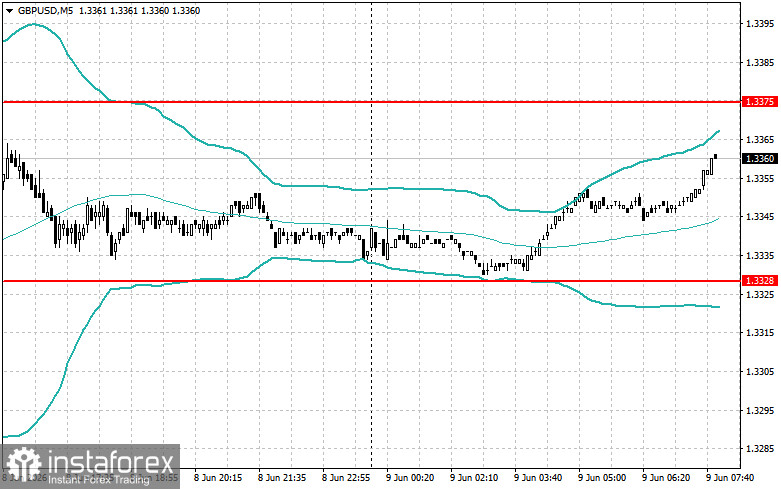

Regarding the pound, there is again no significant data from the UK today, which significantly limits the potential for further recovery of the GBP/USD pair. This lack of macroeconomic indicators means that the market has no new reasons for optimism regarding the British currency, and the pair is likely to remain under pressure.

In this context, yesterday's rise in GBP/USD may quickly come to an end. Without positive news from the British economy, any recovery in the pair will likely be corrective in nature and could be quickly offset by renewed pressure from the dollar.

If the data aligns with economists' expectations, it is best to operate based on the Mean Reversion strategy. If the data comes in significantly above or below economists' expectations, it is best to use the Momentum strategy.