یہ بھی دیکھیں

08.07.2026 09:52 AM

08.07.2026 09:52 AMAll good things come to an end, even the runaway rally in chipmakers. The Philadelphia Semiconductor Index, which just posted its best quarter ever and was up about 74% year-to-date, plunged by more than 4.5%. Even record profits at Samsung Electronics did not stop investors from selling. Yet a majority of S&P 500 constituents still closed in the green — the market chose a rotation over outright capitulation.

The Nasdaq 100 is approaching its seventh consecutive session with moves exceeding 1% in either direction — a sequence not seen since August 2024. Investors are nervous but not stampeding out. Citi argues that positioning in US equities continues to improve thanks to short covering in the S&P 500 and inflows of long-term capital into the Nasdaq 100 and Russell 2000. Neither bulls nor bears have capitulated.

Goldman Sachs takes a different view. The bank believes that capital-intensive businesses are positioned to outperform companies whose value is mainly people and digital goods. Investors still underestimate a landscape in which infrastructure and physical assets regain strategic importance.

UBS remains constructive on the AI growth story and is not abandoning semiconductors, but it warns the next leg of the rally will broaden the list of market leaders. The bank sees the recent pullback as a four-to-six-week flattening, a pause after the rapid April-May advance.

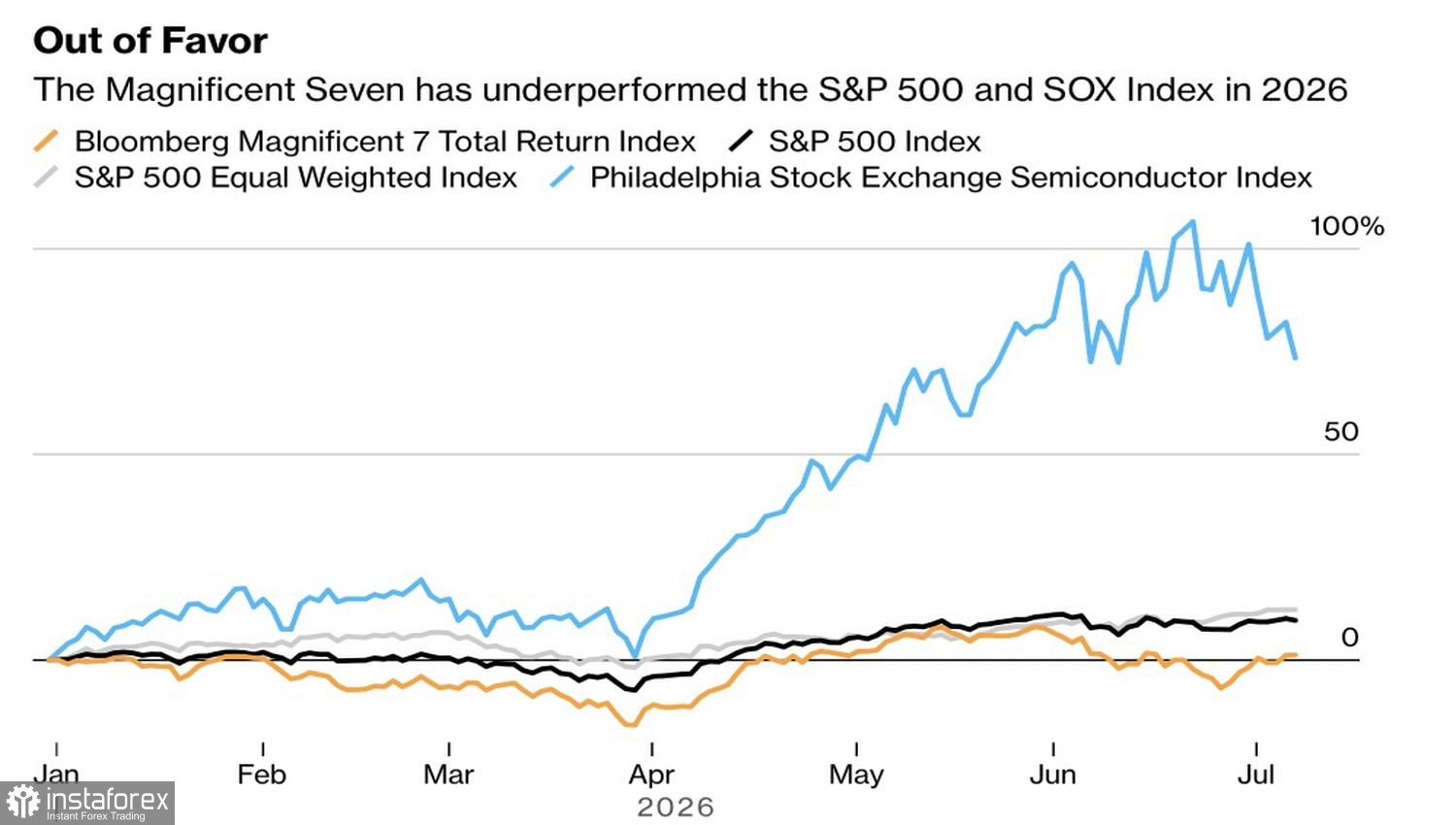

Dynamics of S&P 500, hyperscalers, and chipmakers

Morgan Stanley urges investors to return to the Magnificent Seven: semiconductors are materially overbought, and it is becoming harder to identify the long-term winners in the AI race. The early-year data do not favor the mega-caps: Bloomberg's MAG-7 indicator is up only about 1% year-to-date, while the market-cap-weighted S&P 500 has gained 9.8% and the equal-weighted version 12%.

Earnings season kicks off next week with major bank reports. The main risk is that hyperscalers will fail to meet analysts' inflated expectations for AI capital expenditures.

Geopolitics is back in the foreground. The US Treasury has revoked authorisation for purchases of Iranian oil in response to tanker attacks in the Strait of Hormuz, which pushed Brent toward $76/bbl. Rising inflation expectations have driven Treasury yields higher.

In short, the US equity market is balancing belief in AI with caution ahead of earnings. The rotation into "real" assets could be more than an episode — it may mark the start of a new trend if hyperscalers fail to surprise the market positively.

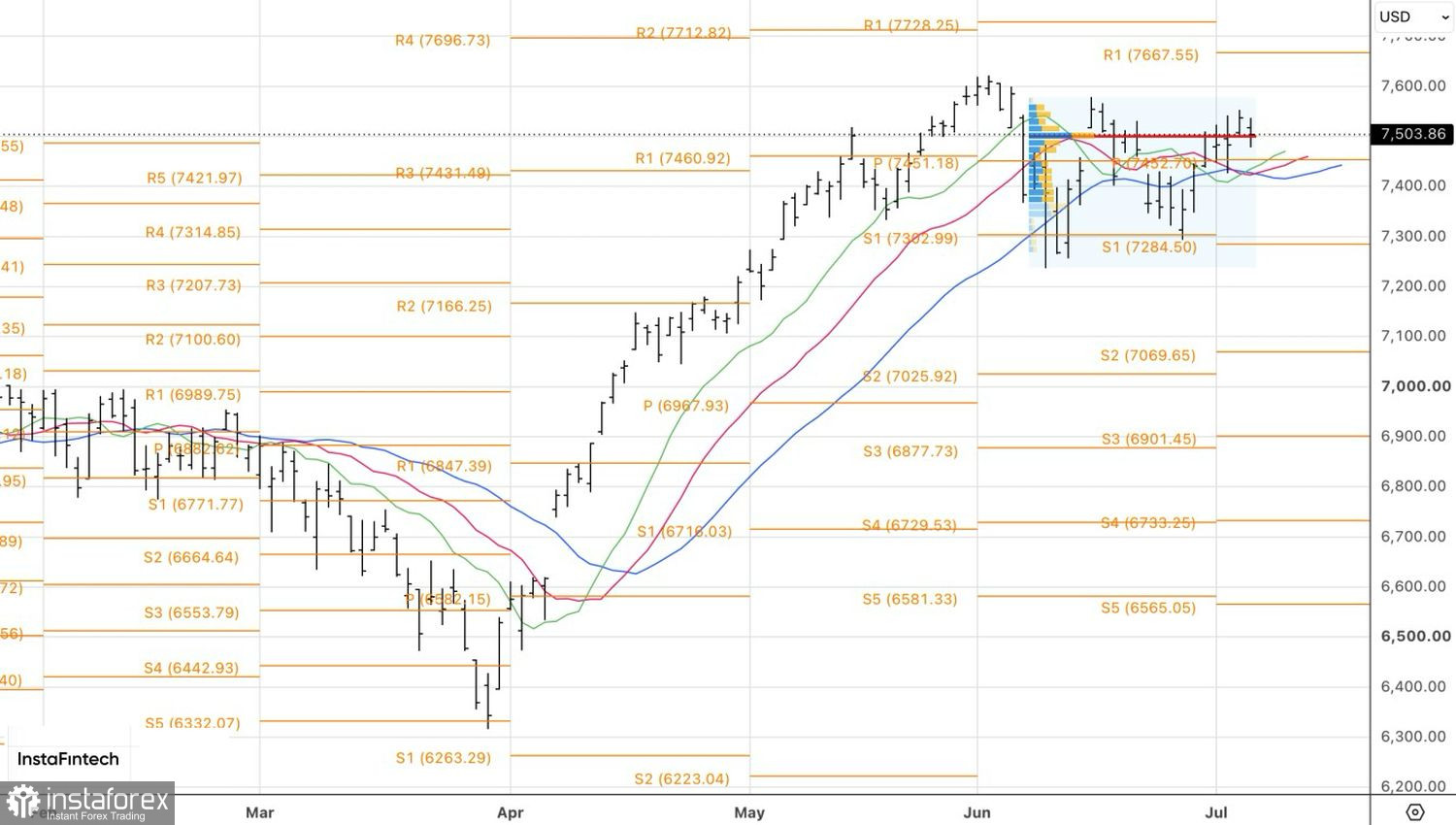

Technically, the daily chart shows that the S&P 500 has returned to a fight around fair value at 7,500. A sustained hold below that level would increase the risk of a pullback and open the door for sales toward 7,370 and 7,290. Conversely, a bull victory would pave the way to build long positions.