See also

25.06.2026 12:56 AM

25.06.2026 12:56 AM

On Wednesday, the EUR/USD pair continued its decline, setting a new annual low.

Support for the U.S. dollar is provided by rising expectations of further monetary policy tightening in the country. Such changes became evident following the recent Federal Reserve meeting, where the central bank's representatives adopted a more "hawkish" stance amid ongoing inflationary pressures.

The dollar is strengthening due to adjustments to the market's interest rate forecasts. Data released last week indicate that an increasing number of Fed members believe a rate hike is necessary by the end of the current year. According to the CME FedWatch tool, investors are confidently pricing in a high probability of rate increases in the coming months, which continues to support the U.S. currency.

This situation contributes to the strengthening of the U.S. Dollar Index (DXY), which has once again reached an annual high, thereby placing pressure on the euro.

Conversely, economic indicators on the European continent are providing some encouraging signals. In June, Germany's IFO business climate index jumped to 85.6 points, up from 85.0 in the previous month, matching analysts' expectations. The current assessment index exceeded forecasts, while the expectations index recorded a moderate improvement. This data confirms a gradual recovery of confidence in the largest economy of the Eurozone.

Experts at Commerzbank note that Germany's economy is likely still experiencing weak growth or even a slight decline in the second quarter due to the impact of high energy prices from the past. However, the bank suggests that the latest results from the IFO survey may indicate the prospects for moderate recovery in the second half of the year.

Additional constraints on the euro's value are imposed by statements from European Central Bank representatives. ECB Chief Economist Philip Lane emphasized that risks remain high despite the improving geopolitical situation in the Middle East, warning that inflation may remain above the 2% target through the first half of 2027. These comments strengthen the view that the ECB will stick to a cautious strategy in the coming months.

Furthermore, the divergence in bond yields between the U.S. and the Eurozone is deepening, putting pressure on the euro. Consequently, the recent adjustment in market expectations toward a more hawkish Fed policy (while expectations for ECB actions remain virtually unchanged) is a key factor acting against the EUR/USD pair in the near term.

Investors are eagerly awaiting the release of the Personal Consumption Expenditures (PCE) price index in the U.S. — a key inflation indicator closely monitored by the Fed — scheduled for publication on Thursday during the North American session. This report has the potential to provide new guidelines for U.S. monetary policy and indicate the subsequent direction of the EUR/USD pair.

From a technical standpoint, the pair is trading below significant moving averages. Oscillators are negative, confirming the bears' advantage. However, it is worth noting that the Relative Strength Index (RSI) has entered the oversold territory, indicating a possible correction. For bulls to regain control of the markets, they need to overcome the 20-day SMA around 1.1542.

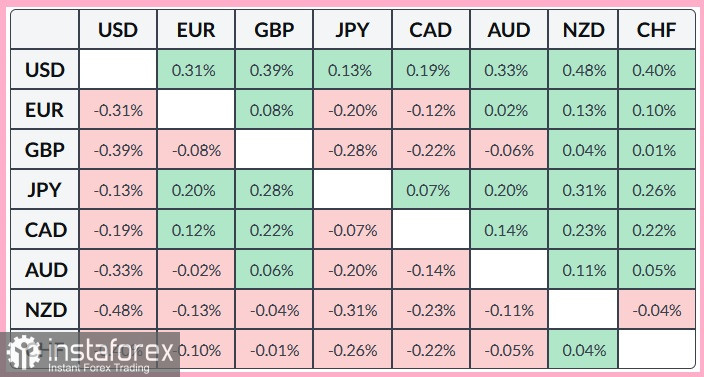

The table below shows the percentage change in the euro exchange rate against selected major currencies for Wednesday. The most significant growth of the euro is observed against the New Zealand dollar.